Author: Anveshi Gutta

Author: Anveshi GuttaThe CFO’s office has always been instrumental in driving strategic decisions and shaping corporate strategy. With Sustainability becoming front and centre in strategic dialogues, the CFO role has become even more compelling. This is relevant for companies equally, irrespective of whether they are adopting sustainability due to regulatory pressure or voluntary actions. For regulatory compliance, it has been considered that the CFO’s office is best suited for sustainability reporting (which in itself, has become significantly quantitative in nature). This is seen as a natural extension to the financial/annual/mainstream reporting, that has conventionally been under the CFO’s purview. The role becomes a lot more relevant when companies take up a 360-degree implementation of sustainability to make it a distinct business advantage.

Through this blog, we delve into the mind of the CFO to understand the challenges that confront him/her today, while putting the sustainability strategy to implementation.

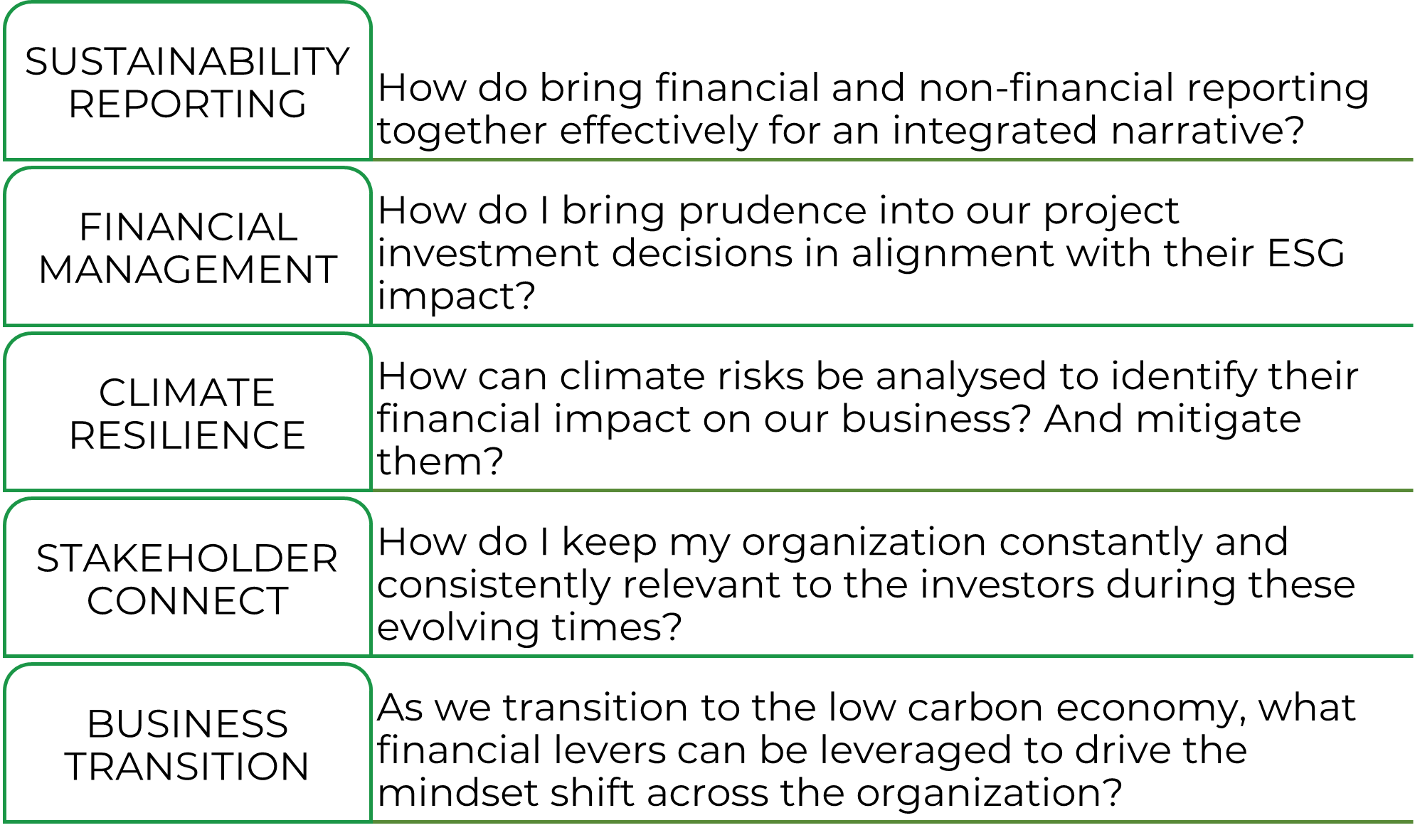

1. How do I bring financial and non-financial reporting together effectively for an integrated narrative?

Financial reporting has been the mainstay of investor relations for a few decades now. These reports have included management commentary and financial statements to address the shareholder and investor community. With the transition being seen from capitalism to stakeholder capitalism, there is a growing demand for non-financial performance reports. At the same time, there is growing pressure from investors to publish ESG metrics. Addressing this requires a seamless amalgamation of financial and non-financial metrics to build an integrated narrative. This will make it easier for the reporting audience to comprehend the results of business operations (financial and impact) better.

We suggest you work with your operational teams on the ground, to ensure that they understand the essence of their role in driving sustainability. In the process, it would be prudent to develop a relevant KPI matrix for your ongoing initiatives, and further, sensitize the on-ground teams towards it. Further, this KPI matrix should mandatorily consider the priorities that are material from both the financial and impact perspectives (also referred to as double materiality).

2. How do I bring prudence into our project investment decisions in alignment with their ESG impact?

Financial decision making within an enterprise is a key function that comes under the purview of the CFO. During business operations, the business teams make tactical financial decisions that are relevant for the scenario at hand. These decisions are usually governed by the guidelines framed by the CFO’s office. At the same time, major decisions around CAPEX are under the direct ownership of the CFO’s office and this is where significant ESG considerations must be brought into screening.

We suggest that ESG assessments are mandatorily done for larger projects. This needs due diligence on the near-term, medium-term and long-term analysis of the projects in the simulated future scenarios. Frameworks that identify the potential outputs, outcomes and impacts of every project, and assess them on both financial value and impact value, need to be framed. This should be additionally supported with Monitoring and Evaluation frameworks to guide the operational teams during the execution of the projects.

3. How can climate risks be analysed to identify their financial impact on our business? And mitigate them?

Climate events and emergencies are far more frequent today. It is imperative that businesses have adequate understanding of the impacts these events have on their core operations. This requires adequate acknowledgement and analysis of climate risks, while ensuring that you are cognizant of the changing environment in the interim. Further, identifying and implementing appropriate risk mitigation measures will help deal with the potential impact in a effective and proactive manner.

We suggest that climate risks be managed as part of the enterprise-wide risk management function, where it exists. Each climate risk needs appropriate analysis on its potential impact, frequency, and likelihood. An important suggestion would be for enterprises to identify both upside and downside risks, so that they do not lose sight of a potential opportunity relevant to its own nature of business. All of this calls for a comprehensive analysis including simulations (at minimum, for the most critical risks) in potential future scenarios (also called Scenario Analysis).

4. How do I keep my organization constantly and consistently relevant to the investors during these evolving times?

The investors’ toolkit has had a significant refresh in recent times. ESG performance criteria is topping their agenda, with each of them realising that it is imperative to generate long-term value while ensuring near-term stability. It is this renewed thinking that requires enterprises to demonstrate their ESG credentials transparently, to earn the attention of the investor community. The CFO’s office has to provide a comprehensive story of past ESG performance while clearly articulating the plans, policies, procedures in place for the consistency to continue in the future.

With your investors becoming increasingly ESG-aware and ESG-mature, we suggest proactively assessing your own ESG performance. This will require adherence to two simple-yet-effective mantras.

- Have adequate measures in place to steer clear of any Greenwashing/ESG-washing, both intentional and unintentional.

- Look beyond ESG from a compliance lens and demonstrate how ESG means business value and stakeholder value.

5. As we transition to the low carbon economy, what financial levers can be leveraged to drive the mindset shift across the organization?

As organizations progressively take up sustainability initiatives aligned with their vision, there is also a need to focus on driving a parallel behavioural shift across teams. There has to be significant top-down guidance across business functions to make this happen. From strategic to tactic decisions, this calls for a planned transition to embed sustainability in your corporate culture. While this may look like a typical HR responsibility, the CFO’s office can play a significant role in addressing this through the KPI framework mentioned earlier.

We suggest that CFO’s office leverages financial levers like Internal Carbon Pricing (ICP), Carbon dividends, Green Finance etc to drive both individual and institutional behavioural shifts. ICP can be used effectively integrated into the budget cycle (planning, allotment, monitoring) to incentivise operations that are carbon-conscious and disincentivize those that aren’t. It must be acknowledged that implementing such financial levers requires a systemic and systematic analysis beforehand, to ensure that there are no loose ends.

With the CFO expected to shoulder significant responsibility during business transition, it is imperative that appropriate support ecosystem is enabled. It is required to refresh the organization’s KPI frameworks, policies and procedures, to bring in sustainability relevant indicators. It is obvious that CFO’s success will drive value creation for a wider range of stakeholders, and in the process, help drive the CEO’s agenda and CSO’s agenda on sustainability.

Watch this short video from Sus360 Bytes that summarises the CFO's Sustainability agenda.